Lately several people have asked me, is “Earnest Capital trying to index early-stage software companies?” The answer is “no, not really” but there is an interesting discussion to be had around the idea of indexing so it’s worth unpacking.

AngelList Data shows that “indexing” early-stage (pre-seed/seed) investing produces superior returns than picking deals.

One reason this is even an idea is that AngelList released a pretty interested white paper about the idea of “indexing” (buying a weighted average basket of all deals versus investing in individual deals). I did a thread reacting to the white paper here:

This paper analyzing @AngelList‘s dataset of seed investments was interesting. Very cool to see them dig into and open up on data. Some thoughts 👇 https://t.co/IGTCgczfQY

— Tyler Tringas (@tylertringas) December 12, 2019

AngelList is a platform for angel investors and now funds to invest in startups and they have a pretty broad dataset of deals. Their data science team ran the numbers and found that if you had invested in a weighted average “index” where you are invested in every credible deal on the platform, you would almost always generate better returns than picking 10, 20, or 50 deals yourself.

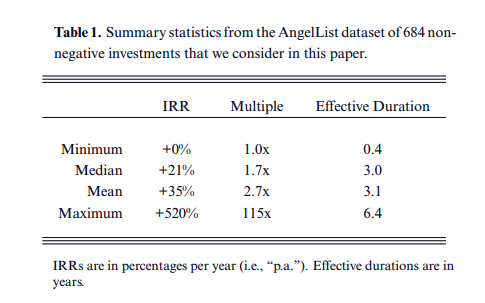

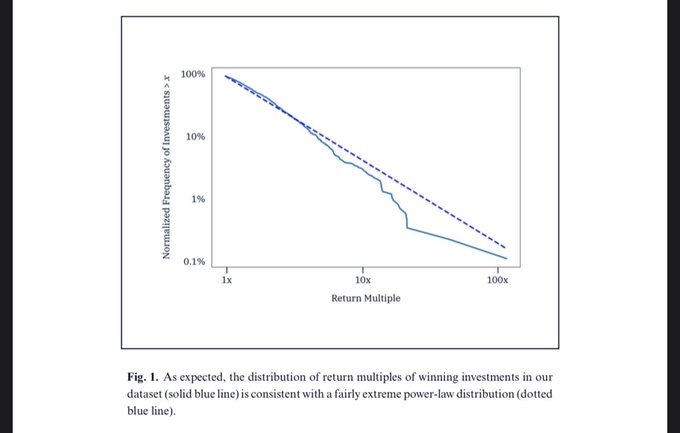

The reason for this effect is the power law: in the AngelList dataset, a huge portion of the total returns to all investors comes from a tiny number of individual investments like Uber, Stripe, Airbnb. Of the 3,000 seed deals, if you missed out on any of these, your portfolio would underperform the index. The more extreme these individual outcomes become, the more the index will beat any individual picker.

Some important caveats:

- They say this only holds true for early stage seed and pre-seed deals, at the later stages this effect goes away.

- Every credible deal is an important distinction. Investing in literally every entrepreneur with an idea would obviously not produce superior returns given the number of bad ideas that never get off the ground. But how to measure “credible” is not at all obvious. A short-hand way to do it is “any deal with an actual VC fund leading the round.” Which to me seems like a better-than-nothing solution but not totally convincing.

Some thoughts on AngelList data

The returns to indexing, while technically better than not indexing, are still not very good and in my opinion don’t clear the hurdle of sufficient return relative to the risk. A reasonable conclusion might be: indexing is better than picking, both produce pretty bad returns, so the best advice is just don’t do angel/early-stage investing.

Returns *excluding* the >50% of investments that fail

These returns exclude all the losing investments that went to zero (at least half). So you can cut these by half to get a general sense of what the actual return to investors is: median of less than 1x your money back, mean of slightly above 1x your back. Not great.

Indexing doesn’t get you any of tangential value of angel investing, which for many people is most of the value:

- Build relationships with smart founders

- Learn a ton via company updates and pitching dealflow

- Potentially get a huge out-sized win

Indexing across a theme

In my opinion the best way to adapt to these realities is to take the idea of indexing and apply it not to “all early-stage startups” but to a specific investing theme or trend that you (a) think is a strong bet and (b) you want to learn more about and plug into.

I think new funds like Andreas Klinger’s Remote First Capital (focused on remote work startups) or Ben Tossell’s new fund focusing on no-code tools and others, would do well to simply adopt an indexing approach: define a thesis of what is/is not in your purview, and write a small check into every credible (has a lead VC) deal that comes your way. This builds the greatest chance to back the right break-out company within a strong thesis, while also accumulating knowledge and expertise about an eco-system. I’ll be curious to see if anybody adopts this approach.

But it all hinges on the power law

The dataset here is not neutral. It is “expected” that they find an extreme power law of outcomes certainly in part because AngelList is a platform for exactly this kind of investing. It’s dominated by Silicon Valley investors and folks who read Naval, Jason Calcanis, and other proponents of the style of investing which is all about backing the next Uber or Airbnb.

A principle bet of Earnest is that power law investing is not a law of physics when it comes to early stage investing. We coined the idea of Early Stage Value Investing, to contrast with the kind of Early Stage Growth Investing that happens on AngelList and in VC. Doing a seed deal and then encouraging the founder to hire aggressively at top tier salaries, hit lofty weekly growth metrics, spend down their seed round in 12-18 months, introducing them to VCs to raise more capital if they can achieve those growth rates… all of this make it both more likely that the company will some day be a unicorn AND more likely that it will fail, making the distributions of outcomes a more extreme power law than if you encouraged a founder to hire cautiously, focus on positive unit economics, and get to profitability quickly. See our Fund 2 thesis for the much longer version of this argument.

So in summary, indexing early-stage beats individual picking if you’re operating in an extreme power law environment, but doesn’t make sense if you’re not.

Does Earnest Capital do indexing?

So coming back to the original question and the answer is No, and this whole discussion is why.

1. We’re not doing power law style investing. We don’t expect, and our strategy isn’t predicated on the idea, that one or two investments will be 90% of our returns. We are maximizing the number of successful entrepreneurs in our portfolio. So the idea that the index will out-perform loses efficacy the less extreme the distribution. The AngelList paper found that in later stage deals, when the distribution of outcomes becomes less extreme, the effect goes away.

2. We’re clearly doing something much closer to active management / picking. In doing our first 20 investments, we looked at over 2,000 opportunities. Yes I know this is a vanity metric, but it’s relevant here because we’re just obviously not “indexing” this market with that kind of ratio. We could probably have invested in ~100 of those with more capital, but a very large number of the opportunities were not viable investments (or at least not yet).

3. There really is no benchmark for credible deals in our space. Public stock indices need the public market traders (and subsequent market caps) to know which companies to include in the index. Indexing requires some sort of external form of validation. In our market the only thing comparable would be customer revenue, which is is a great form of validation but there are still plenty of businesses that get to $1k-5k in MRR that wouldn’t make for great investments. We have to be our own form of validation (maybe some day somebody will index us with a Fund of Funds?). Essentially, you can’t index something that doesn’t already have a robust market of active managers creating a good threshold for credibility and that is definitely not the case in the “funding for bootstrappers” market.

So we don’t do indexing. We’re actively betting on the opportunities we think are most likely to succeed. So far that’s going pretty well but we’ve got a lot of ways to get better too.